Recession risks loom larger

Genevieve Signoret

(Hay una versión en español de este artículo aquí.)

Our confidence for the global economy in 2022–2023 is weakening. We revise up our projections for inflation in the United States and Mexico but also the risk of recession, thus revise down the speed at which we expect the Fed to raise rates. We throw out our upside risk scenario.

We revise up our forecast for US inflation

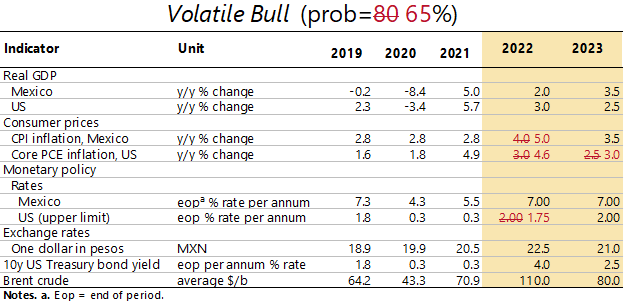

Core PCE inflation in the United States is trending up. commodity prices and in particular fuel prices are exploding. Thus, we revise up our central-scenario forecast for core PCE inflation in 2022 to 4.6% from 3.0%, and for 2023 to 3.0% from 2.5%.

The uptick in U.S. core PCE inflation is one factor prompting us to revise our U.S. inflation forecast up to 4.6%

We revise down our forecast for the speed of Fed tightening

Having just read of our upward revision to our inflation outlook, you may be expecting us to report, further, an upward revision to our projection for the speed at which the Fed will hike rates this year. In fact, we instead revise that projection down: we now expect the Fed to move more slowly than we were anticipating not long ago.

Oil price shocks are negative for growth. In the short run, demand for oil is rather price-insensitive. Until consumers can adjust their lifestyles—and businesses can adjust their processes—to cut down on hydrocarbon use, consumers are likely to respond to higher fuel prices by cutting back on discretionary spending, and businesses by cutting back on production and thus spending on non-energy inputs.

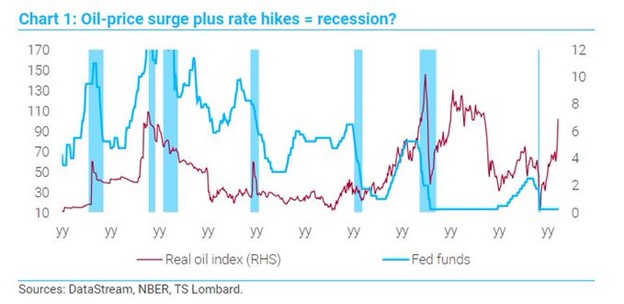

Fed policy makers know this. And are painfully aware that oil price shocks followed by tightening have always led to recessions, as shown in this graph from Dario Perkins at TS Lombard:

We thus revise down our outlook for the upper limit on the target federal funds rate to 1.75% by year end from our earlier 2.00%.

We revise up our perceived risk of recession

Now, our revised Fed outlook does not mean that we’re sure that the Fed can thereby bring the U.S. economy to a soft landing. It would be a first. Also, today’s oil price shock is more negative for global growth than prior ones, because it’s posing risk to financial stability. The war in Ukraine and resulting sanctions on Russia have driven up prices not only for oil but also for a slew of commodities. This is destabilizing the commodities derivatives market, posing a risk of contagion to other market segments.

Furthermore, sanctions on Russia are causing global banks and non-financial businesses to mark down (often to zero) the value of their Russia-linked assets. The resulting harm to balance sheets poses an additional risk of contagion.

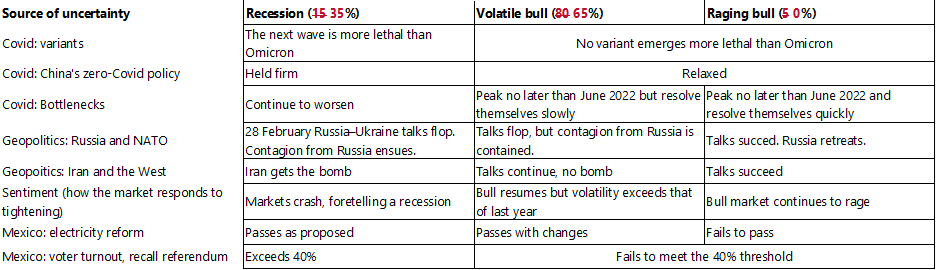

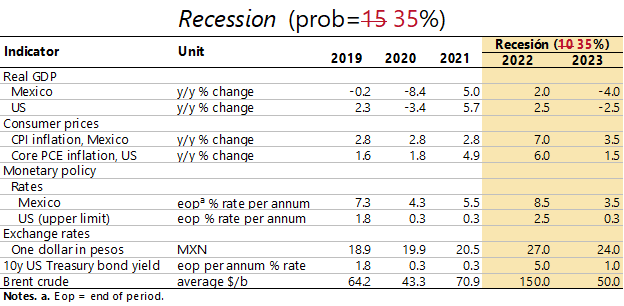

Because of the Fed’s history of failures to achieve soft landings in response to oil shocks and because of the aforementioned risks of contagion, we no longer see any chance that our upside risk scenario will play out. We have thrown it out. And we now see a 35% risk that the U.S. and world economies will fall into recession this year or next. This is up from our earlier perception that the risk was 15%.

We had to throw out our upside risk scenario, and we now see the probability that the U.S. and the world will enter recession next year to 35% from our earlier 15%

We revise up our forecast for inflation in Mexico

Finally, based on Mexico’s latest inflation numbers showing core inflation continuing to trend up, we again revise up our forecast for Mexican headline consumer price inflation to 5.0% from our earlier 4.0%.

In Mexico, month-on-month core inflation continues to trend up; we now see inflation for all of 2022 reaching 5%

We throw out our upside risk scenario

We summarize our updated views in the following forecast tables for our only two remaining scenarios, the one we still see as more probable, Volatile Bull, and our downside risk scenario, Recession.

Research assistance by Estefanía Villeda. Editing by Andrés Aranda.