Global macro forecast 2016–2017: “Finesse”

Genevieve Signoret

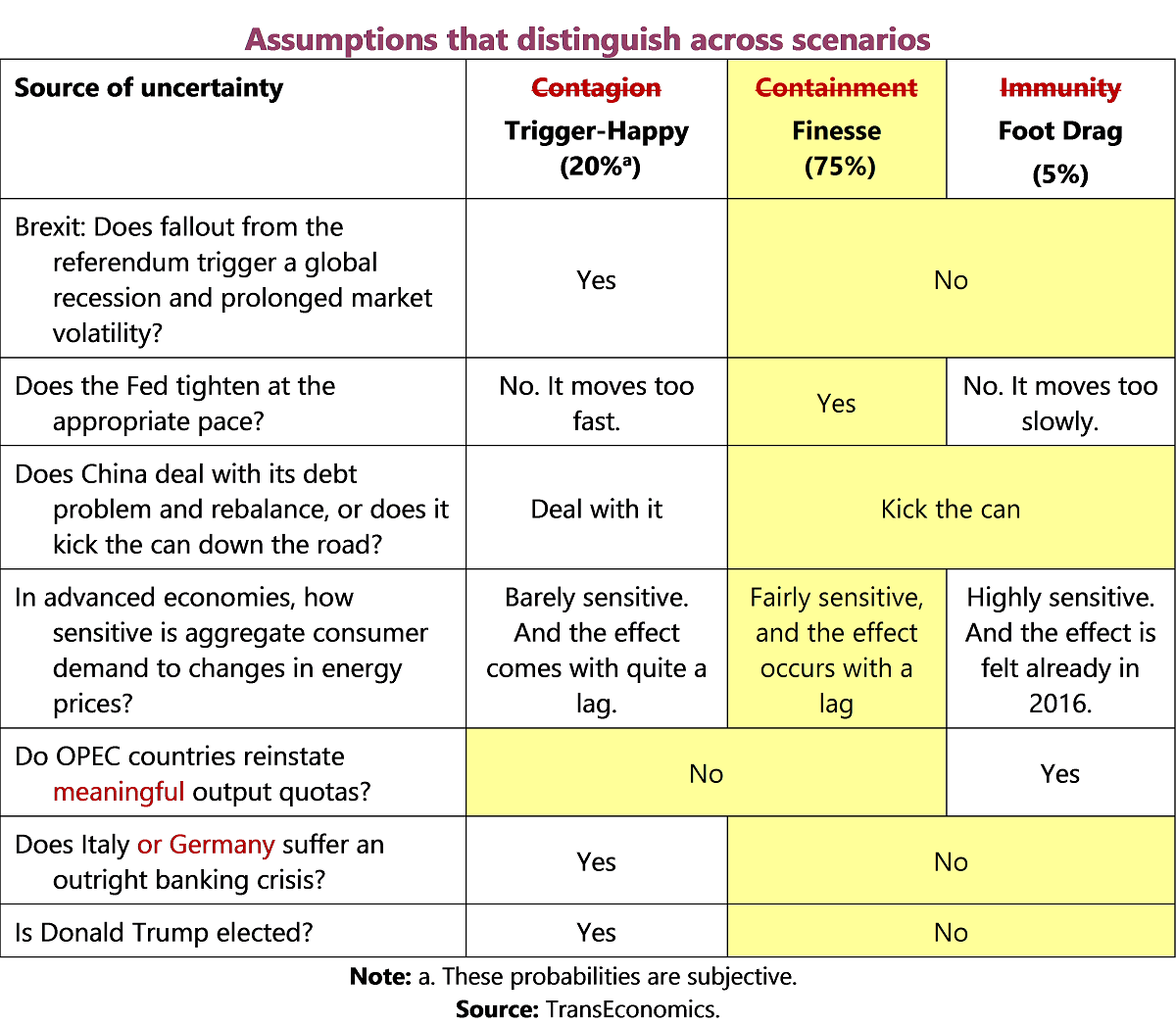

We update our global macro forecast under three scenarios. We hold to our forecast scenario assumptions but adopt new scenario names. We now called our central scenario Finesse in reference to the two greatest market risks looming today: first, that the Fed will fail to finesse its policy normalization program and hence either derail growth (by hiking rates too early) or set off high inflation (by hiking rates too late); second, that Chinese authorities will fail to finesse their efforts to deflate, in orderly fashion, China’s credit bubble, and hence either move China into immediate recession (by moving too abruptly and too aggressively to dry up credit flows) or sow the seeds for a major crisis in the medium term (by kicking the can too far down the road).

In our central scenario, we assume that both risks are averted. We further assume that Brexit implementation and the macro-market fallout it causes, though unpleasant, are orderly. Donald Trump loses the U.S. presidential election. Italy and Germany avert banking crises. Consumer demand in advanced economies is only moderately sensitive to oil price movements. And any agreement that OPEC manages to reach and enforce gives no better than a weak boost to crude oil prices.

Under these assumptions, the global economy continues to grow slowly despite nearly flat trade and manufacturing, inflation rates remain low, interest rates barely move up in the USA and emerging markets while remaining at or below zero in Japan and Western Europe. The European Central Bank and the Bank of Japan step up quantitative easing. The euro and yen depreciate against the U.S. dollar, while the Mexican peso appreciates. Average oil prices increase just a bit. The bull market continues but legitimate jitters over high U.S. stock market valuations along with Fed normalization talk and action continue to strengthen demand for emerging market stocks relative to demand for U.S. stocks.

We assign to Finesse a subjective probability of 75%.

Our downside risk scenario is called Trigger-Happy (probability=20%): the Fed and the Chinese authorities move too aggressively too fast, causing a global recession (5%) in 2017. Our upside risk scenario is called Foot Drag: the Fed and Chinese authorities postpone for too long policy moves too weak, building euphoria in the short run while sowing the seeds for a medium-term burst of inflation in the USA and recession with financial crisis in China. By “medium-term”, we mean in 2018 or beyond.

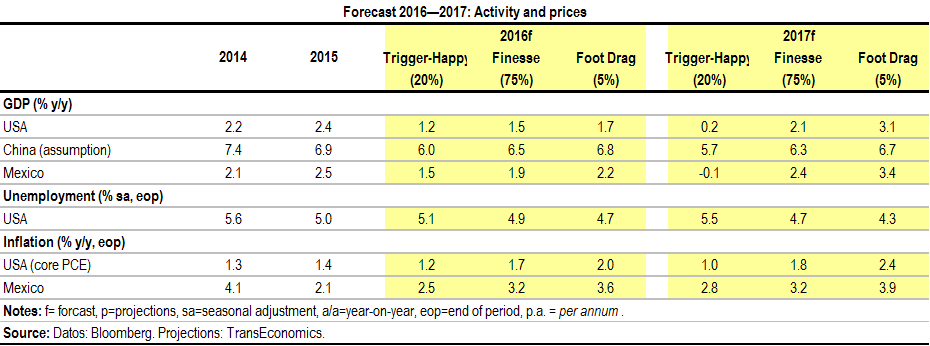

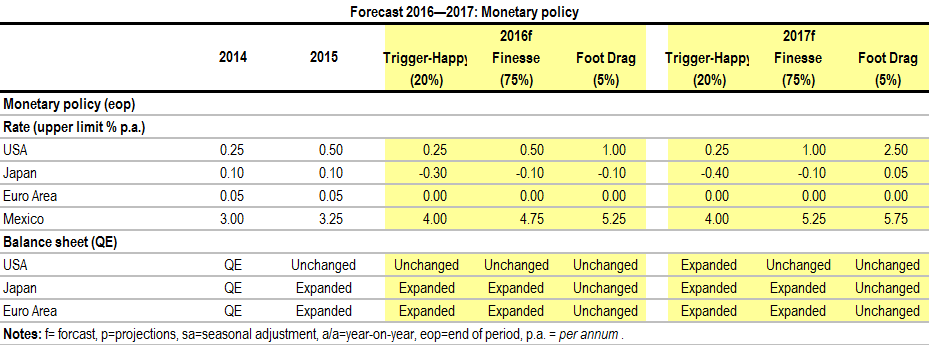

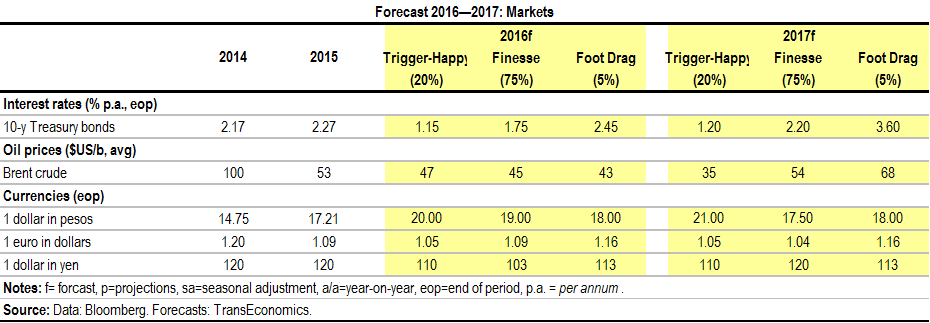

We summarize these forecast assumptions and present our forecast numbers in the following tables:

To zoom in on any of the following forecast tables, please click on the table.